Fill Out a Valid Connecticut 8379 Template

Fill Out a Valid Connecticut 8379 Template

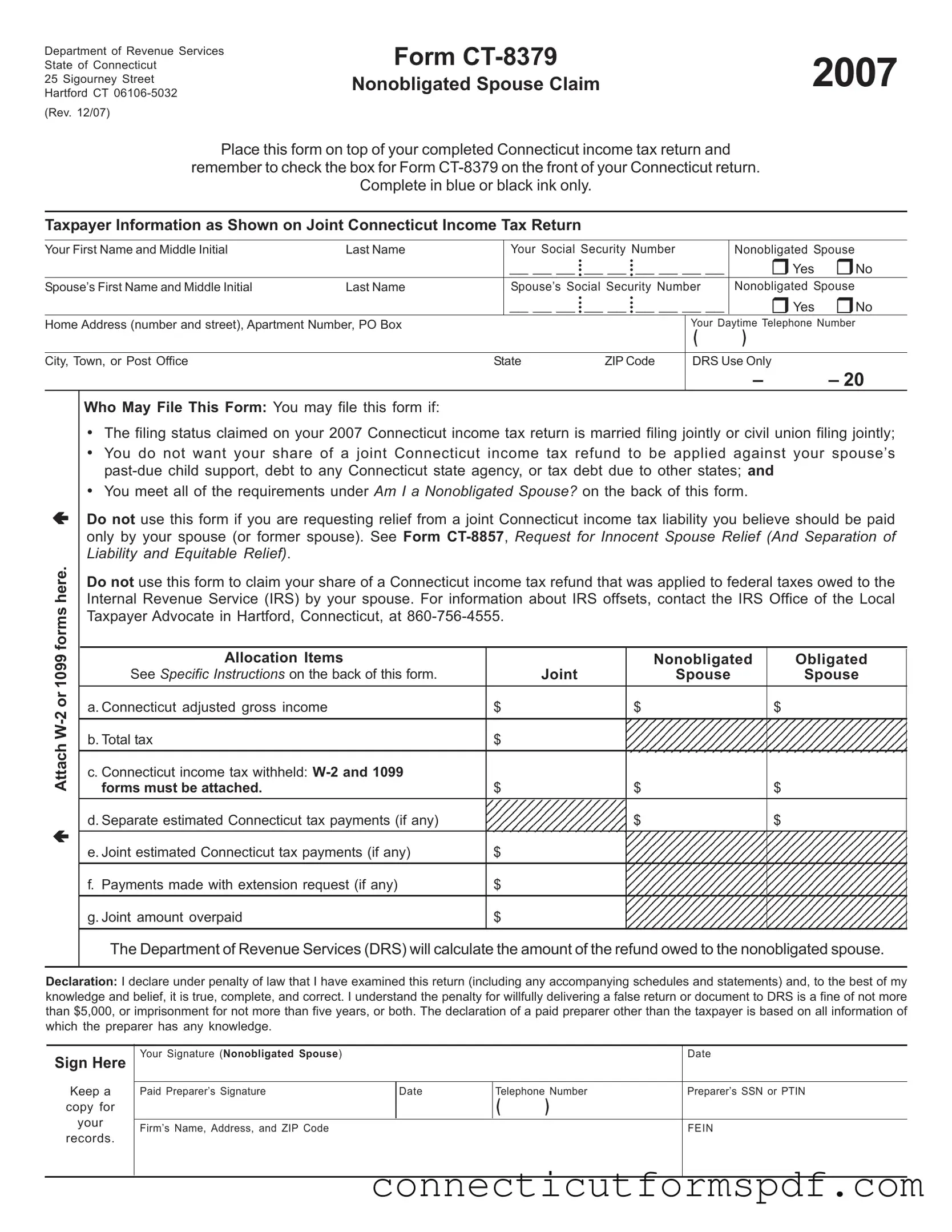

In the realm of Connecticut's tax procedures, Form CT-8379 emerges as a crucial document for married couples or civil union partners who have filed their income tax returns jointly but seek to protect their rightful share of a tax refund from being applied towards their spouse's debts. This unique form, designed by the Department of Revenue Services, serves as an assertion of rights by the nonobligated spouse—that is, the partner who does not bear responsibility for their spouse's debts, including past-due child support, state agency debts, or tax obligations to other states. Crucially, the form allows individuals to lay claim to their portion of the tax refund, ensuring that it is not automatically diverted to settle the financial liabilities of the obligated spouse. Applicants are required to meticulously complete this form, providing comprehensive details of their joint tax contributions, income, and the specific portions subject to refund allocation, while attaching relevant W-2 and 1099 forms to substantiate their withholding amounts. The declaration section mandates a signatory acknowledgment from the nonobligated spouse, attesting to the accuracy and completeness of the information provided, under penalty of law. Additionally, it outlines the procedural aspects of filing, including the necessity to check the designated box on the Connecticut income tax return form and the placement of Form CT-8379 atop the tax return submission stack, thereby simplifying the process for the Department of Revenue Services to identify and process these claims effectively. This underscores the form's significance in safeguarding individuals' financial interests, preventing unintended allocation of their tax refunds towards their spouse’s liabilities, and highlighting the state's acknowledgment of each individual's fiscal autonomy within a marital or civil union framework.

Department of Revenue Services

State of Connecticut

25 Sigourney Street

Hartford CT

(Rev. 12/07)

Form |

2007 |

Nonobligated Spouse Claim |

Place this form on top of your completed Connecticut income tax return and

remember to check the box for Form

Complete in blue or black ink only.

Taxpayer Information as Shown on Joint Connecticut Income Tax Return

Your First Name and Middle Initial |

Last Name |

|

Your Social Security Number |

|

Nonobligated Spouse |

|||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

Nonobligated Spouse |

|

Spouse’s First Name and Middle Initial |

Last Name |

|

Spouse’s Social Security Number |

|||||

|

|

|

• |

• |

__ __ __ __ |

Yes |

No |

|

|

|

|

__ __ __ •• |

__ __ •• |

||||

|

|

|

• |

• |

|

|

|

|

Home Address (number and street), Apartment Number, PO Box |

|

|

|

|

Your Daytime Telephone Number |

|||

|

|

|

|

|

|

( |

) |

|

|

|

|

|

|

|

|

|

|

City, Town, or Post Office |

|

State |

ZIP Code |

DRS Use Only |

|

|||

|

|

|

|

|

|

|

– |

– 20 |

Attach

Who May File This Form: You may file this form if:

•The filing status claimed on your 2007 Connecticut income tax return is married filing jointly or civil union filing jointly;

•You do not want your share of a joint Connecticut income tax refund to be applied against your spouse’s

•You meet all of the requirements under Am I a Nonobligated Spouse? on the back of this form.

Do not use this form if you are requesting relief from a joint Connecticut income tax liability you believe should be paid only by your spouse (or former spouse). See Form

Do not use this form to claim your share of a Connecticut income tax refund that was applied to federal taxes owed to the Internal Revenue Service (IRS) by your spouse. For information about IRS offsets, contact the IRS Office of the Local Taxpayer Advocate in Hartford, Connecticut, at

|

Allocation Items |

|

Nonobligated |

Obligated |

|

See Specific Instructions on the back of this form. |

Joint |

Spouse |

Spouse |

|

|

|

|

|

|

a. Connecticut adjusted gross income |

$ |

$ |

$ |

|

|

|

|

|

|

b. Total tax |

$ |

|

|

|

|

|

|

|

|

c. Connecticut income tax withheld: |

|

|

|

|

forms must be attached. |

$ |

$ |

$ |

|

|

|

|

|

|

d. Separate estimated Connecticut tax payments (if any) |

|

$ |

$ |

|

|

|

|

|

|

e. Joint estimated Connecticut tax payments (if any) |

$ |

|

|

|

|

|

|

|

|

f. Payments made with extension request (if any) |

$ |

|

|

|

|

|

|

|

|

g. Joint amount overpaid |

$ |

|

|

|

|

|

|

|

The Department of Revenue Services (DRS) will calculate the amount of the refund owed to the nonobligated spouse.

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to DRS is a fine of not more than $5,000, or imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Sign Here

Keep a

copy for

your

records.

Your Signature (Nonobligated Spouse) |

|

|

|

Date |

|

|

|

|

|

Paid Preparer’s Signature |

Date |

Telephone Number |

Preparer’s SSN or PTIN |

|

|

|

( |

) |

|

|

|

|

|

|

Firm’s Name, Address, and ZIP Code |

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

Form

Purpose: Use Form

•You are a nonobligated spouse and all or part of your overpayment was (or is expected to be) applied against:

•Your spouse’s past due State of Connecticut debt (such as child support, student loan, or any debt to any Connecticut state agency); or

•A tax debt due to other states; and

•You want your share of the joint overpayment refunded to you.

Any reference in this document to a spouse also refers to a party to a civil union recognized under Connecticut law.

General Instructions

Am I a Nonobligated Spouse?

You are a nonobligated spouse, if you meet all of the following requirements:

•You filed a joint Connecticut income tax return with a spouse who owes

•You received income (such as wages, interest, etc.) reported on the joint return;

•You made Connecticut income tax payments (such as withholding or estimated tax payments) reported on the joint return;

•You do not owe

•You filed a joint return reporting an overpayment of Connecticut income tax, all or part of which was or is expected to be applied against

Filing the Return: You must file Form

You must place this form on top of the completed Connecticut income tax return. If you previously filed your 2007 Connecticut income tax return, mail this form separately to: Department of Revenue Services, PO Box 5035, Hartford CT

Important: Attach copies of all forms

showing Connecticut income tax withheld to Form CT- 8379.

Specific Instructions

Taxpayer Information: Enter the taxpayer information exactly as it appears on your Connecticut income tax return. The name and Social Security Number (SSN) entered first on the joint tax return must also be entered first on Form

Allocation Items

a.Connecticut adjusted gross income: Enter the joint amount as reported on your joint Connecticut income tax return (Form

Nonresidents and

Nonresidents and |

Connecticut Source Income |

|

(Form |

||

Only |

||

|

Allocation Item

Joint

Nonobligated Spouse

Obligated Spouse

b.Total tax: Enter the joint Connecticut tax liability as reported on your joint Connecticut income tax return (Form

c.Connecticut income tax withheld: Enter the joint Connecticut withholding as reported on your joint Connecticut income tax return (Form

d.Separate estimated Connecticut tax payments: Enter any separately paid estimated Connecticut income tax payments in the appropriate spaces.

e.Joint estimated Connecticut tax payments: Enter the total amount of any joint estimated Connecticut income tax payments. Include overpayments applied from a previous year.

f.Payments made with extension request: Enter the joint amount as reported on your joint Connecticut income tax return (Form

g.Joint amount overpaid: Enter the joint amount overpaid as reported on your joint Connecticut income tax return (Form

Nonobligated Spouse Refund: DRS will calculate the amount of the nonobligated spouse’s refund. The nonobligated spouse’s share of the joint Connecticut tax overpayment cannot exceed the joint overpayment.

Signature: The nonobligated spouse must sign this form.

Others Who May Sign for the Nonobligated Spouse: Anyone with a signed Power of Attorney may sign on behalf of the nonobligated spouse. Attach a copy of the Power of Attorney.

Paid Preparer’s Signature: Anyone you pay to prepare your return must sign and date it. Paid preparers must also enter their SSN or Personal Tax Identification Number (PTIN), and their firm’s Federal Employer Identification Number (FEIN) in the spaces provided.

Form

| Fact | Detail |

|---|---|

| Form Number | CT-8379 |

| Title | 2007 Nonobligated Spouse Claim |

| Issuing Body | Department of Revenue Services State of Connecticut |

| Revised Date | December 2007 |

| Purpose | For a nonobligated spouse to claim a share of a joint Connecticut income tax refund that was or is expected to be applied towards the obligated spouse's debts |

| Eligibility | Married filing jointly or civil union filing jointly and not wanting joint refund to be applied against spouse’s debts |

| Key Requirements | Filing a joint return with an obligated spouse and reporting joint overpayment |

| Required Attachments | Copies of all forms W-2 and 1099 showing Connecticut income tax withheld |

| Governing Law | Connecticut state law |

| Submission Instructions | File with Connecticut income tax return, placing this form on top; if already filed, mail separately to DRS |

Filing Form CT-8379, also known as the Nonobligated Spouse Claim, involves submitting essential information about yourself and the joint tax return you filed with your spouse. This procedure is crucial for ensuring that your portion of any tax overpayment is refunded to you instead of being used to settle your spouse's outstanding debts. Accuracy and attention to detail are vital throughout this process.

By meticulously following these instructions, you can successfully submit Form CT-8379, ensuring that your rights as a nonobligated spouse are protected. This form is a declaration of your request to have your portion of the joint tax refund issued directly to you, bypassing any claims on the refund due to your spouse's debts.

Who is eligible to file Form CT-8379 in Connecticut?

Individuals who are married or in a civil union and filed a joint Connecticut income tax return can use Form CT-8379. This form is specifically designed for those wishing to prevent their share of the joint tax refund from being used to cover their spouse's debts, such as past-due child support, any debt to Connecticut state agencies, or tax debts owed to other states. It's important to note, however, that this form shouldn't be utilized by those seeking relief from joint tax liability that they believe should be solely the responsibility of their spouse.

What are the requirements to be considered a nonobligated spouse?

To be regarded as a nonobligated spouse, several criteria must be met. Firstly, you must have filed a joint tax return with a spouse who has existing debts, such as overdue child support or state debts. Additionally, you must have reported income on this joint return and have made Connecticut income tax payments. Importantly, you should not owe any back payments for child support, state agency debts, or taxes to other states. The joint return must report an overpayment, part or all of which is at risk of being applied to the spouse’s debts.

How should Form CT-8379 be filed?

Form CT-8379 should be filed along with your Connecticut income tax return. Remember to indicate on your tax return that you have included Form CT-8379. Place it on top of your completed tax return paperwork. If you have already filed your tax return for the year without this form and wish to submit it subsequently, it should be mailed separately to the designated address for the Department of Revenue Services. It is also essential to attach copies of all W-2 and 1099 forms showing Connecticut income tax withheld.

What kind of information and allocations are required on Form CT-8379?

The form requires detailed information about both spouses, including Social Security numbers and the allocation of income, tax withholdings, and estimated payments between the obligated and nonobligated spouses. Specific sections necessitate detailing income sources, tax liability, withholding amounts, any separate or joint estimated tax payments, and details of any payments made with an extension request. It is vital that separate allocations are accurately calculated and reported to ensure the correct refund amount is issued to the nonobligated spouse.

Who signs Form CT-8379, and is a preparer's signature necessary?

The nonobligated spouse is required to sign Form CT-8379. In cases where the nonobligated spouse cannot sign the form themselves, someone holding a valid Power of Attorney can sign on their behalf. Should this be the case, a copy of the Power of Attorney documentation must be attached. If the tax return and form were prepared by a professional for a fee, the paid preparer is also required to sign and date the form, providing their Social Security Number (SSN) or Personal Tax Identification Number (PTIN), as well as their firm’s Federal Employer Identification Number (FEIN), ensuring full compliance and accountability.

Filling out Form CT-8379 in Connecticut can be daunting, and mistakes can inadvertently occur. Understanding these common errors can help ensure that your Nonobligated Spouse Claim is processed smoothly and efficiently.

Firstly, a prevalent mistake involves not including the correct taxpayer information as it appears on your joint Connecticut income tax return. This includes the full name and Social Security Number for both spouses. It's crucial that this information is entered accurately and corresponds exactly with the information on your joint return. Any discrepancy in this section can lead to delays or the rejection of the form.

Another area where errors frequently happen is in the allocation of items such as Connecticut adjusted gross income, total tax, and Connecticut income tax withheld. Each of these items must be meticulously divided between the nonobligated and obligated spouse. It is essential to ensure that the sum of the individual incomes equals the reported joint income. Similarly, tax liabilities and withholdings must be accurately listed for both spouses as per their individual contributions.

Following these guidelines can significantly reduce the chances of encountering issues during the processing of your claim. Ensuring the accuracy and completeness of your submission not only facilitates a smooth process but also helps in securing your rightful claim without unnecessary delays.

In conclusion, while filling out Form CT-8379 might seem straightforward, attention to detail is key. Simple oversights can complicate or prolong the process. Therefore, carefully reviewing your form before submission is essential. Remember, the goal is to protect your rights and ensure your share of any joint tax overpayment is properly refunded to you.

Filing Form CT-8379, the Nonobligated Spouse Claim, within the State of Connecticut, is a crucial step for those who wish to have their portion of a joint tax refund protected from being directed towards satisfying the tax liabilities or debts of their spouse. To ensure a smooth process and bolster the case for a rightful refund allocation, several other forms and documents might accompany this form. Each document has its own role in painting a fuller picture of the financial landscape and the justice of the claim being made.

Understanding and gathering these forms and documents before initiating the submission of Form CT-8379 can significantly expedite the review process, ensuring the nonobligated spouse's rights are upheld efficiently. It's about more than just filling out paperwork; it's about securing one's financial independence and asserting rightful claims within the legal and tax framework of the State of Connecticut.

The Connecticut 8379 form, known as the Nonobligated Spouse Claim, finds its likeness in several other forms across various tax stipulations and scenarios, primarily aimed at addressing concerns between spouses under specific financial conditions. One such document worth mentioning in this context is the IRS Form 8379, Injured Spouse Allocation. While the IRS Form 8379 serves a broader, federal purpose, it shares the Connecticut form's goal of protecting the financial interests of a spouse unaffected by the other spouse's debt liabilities, including child support, student loans, or federal tax debts. Both forms require detailed financial information from the filers, aiming to ensure that the nonobligated or injured spouse's portion of any tax refund is rightly allocated to them, rather than being used to offset the obligated spouse's debts. The process demands a detailed allocation of income, tax liabilities, payments, and refunds.

Another document closely related in function to the Connecticut Form CT-8379 is the Form CT-8857, Request for Innocent Spouse Relief (And Separation of Liability and Equitable Relief). Though not identical, Form CT-8857 intersects with CT-8379 in its focus on providing relief to spouses not responsible for a tax debt arising from joint tax filings. Form CT-8857 is designed for those seeking relief from joint tax liabilities, under the premise that holding them accountable for such debts would be unfair or inequitable. This form caters to situations where a spouse or former spouse failed to report income, reported income improperly, or claimed improper tax deductions or credits without the knowledge of the innocent spouse, leading to understated tax liabilities. It represents a broader scope of relief by addressing tax liabilities beyond mere refund offsets, which is the primary focus of Form CT-8379.

Filing Form CT-8379, the Nonobligated Spouse Claim, is a critical process for protecting your portion of a joint income tax refund from being applied to debts owned solely by your spouse. It is crucial to adhere to specific do's and don'ts to ensure the form is filled out correctly and efficiently.

Things You Should Do:

Things You Shouldn't Do:

By diligently following these guidelines, you can effectively file Form CT-8379 and safeguard your contribution to any overpayment of Connecticut income tax from being used to offset your spouse’s debts.

Many people have misunderstandings about Form CT-8379, the Nonobligated Spouse Claim in Connecticut. Here are seven common misconceptions and clarifications to help you understand the form better:

Understanding these key points about Form CT-8379 can help you navigate the process of filing it correctly and set realistic expectations about its outcome.

Here are key takeaways regarding the completion and use of the Connecticut Form CT-8379:

Using Form CT-8379 accurately ensures that individuals who meet the criteria as nonobligated spouses can claim their rightful share of a tax refund, without it being automatically applied to their spouse's liabilities.

Connecticut Sba 2 - Important for CPAs in Connecticut wanting official registration for their certificate and the rights to use the CPA title accordingly.

How to File for Full Custody in Ct - Targets the legal prerequisites for applying for custody or visitation in Connecticut, guiding parents through the gathering of necessary documentation.

Coaching Certification Ct - The form includes an attestation section where the applicant must sign, certifying all information provided is true.