Fill Out a Valid Connecticut Au 463 Template

Fill Out a Valid Connecticut Au 463 Template

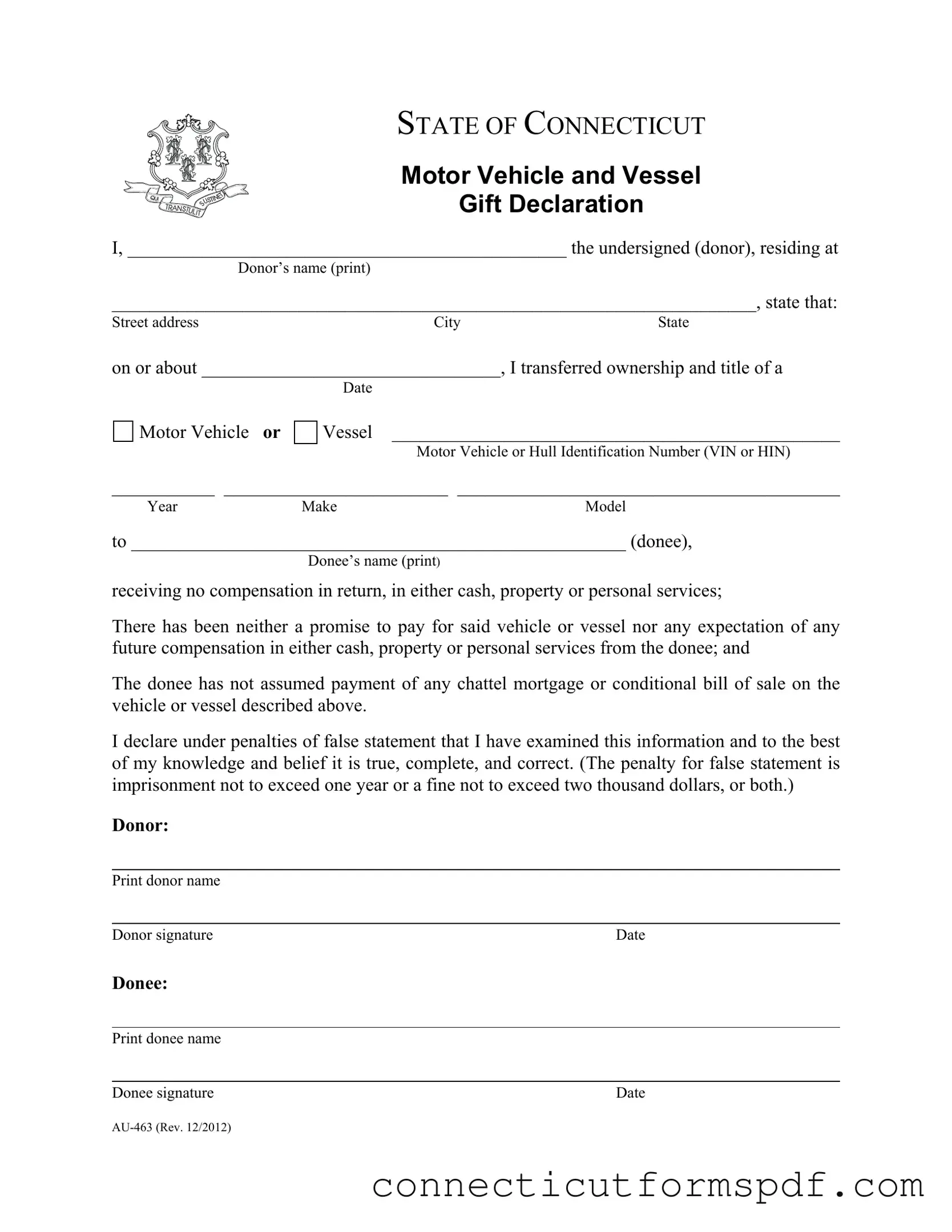

Navigating the processes involved in the transfer of ownership for motor vehicles and vessels in Connecticut can be complex, yet the Connecticut Au 463 form simplifies this procedure by allowing the transfer to be recognized as a gift. Designed as a declaration, this form plays a crucial role in legally documenting the act of giving a motor vehicle or vessel from one person (the donor) to another (the donee) without any compensation exchanged. It covers essential information such as the names and addresses of both the donor and the donee, the transfer date, and detailed information about the vehicle or vessel, including its year, make, model, and identification number (VIN or HIN). Crucially, the form establishes that the gift is made without any expectation of payment or compensation in any form, ensuring that the transaction cannot be misconstrued as a sale. The signing of this document under penalty of false statement - with consequences of imprisonment or a fine for dishonesty - underscores the importance of the integrity of the information provided. By completing the Au 463 form, parties can transparently communicate their intentions to the State of Connecticut, promoting a smooth transfer process while adhering to state regulations.

STATE OF CONNECTICUT

MOTOR VEHICLE AND VESSEL

GIFT DECLARATION

I, _______________________________________________ the undersigned (donor), residing at

Donor’s name (print)

_____________________________________________________________________, state that:

Street addressCityState

on or about ________________________________, I transferred ownership and title of a

Date

Motor Vehicle OR

Vessel ________________________________________________

Motor Vehicle or Hull Identification Number (VIN or HIN)

___________ ________________________ _________________________________________

YearMakeModel

to _____________________________________________________ (donee),

Donee’s name (print)

receiving no compensation in return, in either cash, property or personal services;

There has been neither a promise to pay for said vehicle or vessel nor any expectation of any future compensation in either cash, property or personal services from the donee; and

The donee has not assumed payment of any chattel mortgage or conditional bill of sale on the vehicle or vessel described above.

I declare under penalties of false statement that I have examined this information and to the best of my knowledge and belief it is true, complete, and correct. (The penalty for false statement is imprisonment not to exceed one year or a fine not to exceed two thousand dollars, or both.)

DONOR:

Print donor name

Donor signature |

Date |

DONEE:

Print donee name

Donee signature |

Date |

| Fact Name | Detail |

|---|---|

| Form Identification | AU-463 |

| Revision Date | December 2012 |

| Purpose | Motor Vehicle and Vessel Gift Declaration |

| Applicability | Used in the State of Connecticut for the transfer of ownership and title of a motor vehicle or vessel as a gift |

| Required Information | Donor and donee’s names and addresses, description of the gifted vehicle or vessel (Year, Make, Model, VIN or HIN), and signatures |

| Key Declaration | The donor states that the transfer of the vehicle or vessel was made without receiving any compensation in return |

| Condition | No promise of payment nor expectation of future compensation for the gifted vehicle or vessel |

| Penalty for False Statement | Imprisonment not to exceed one year, a fine not to exceed two thousand dollars, or both |

| Governing Law | Connecticut State Law |

Filling out the Connecticut Au 463 form is a straightforward process that involves providing specific details about the transaction between the donor (the person giving the vehicle or vessel) and the donee (the recipient of the gift). This form is a legal document that declares the transfer of ownership of a motor vehicle or vessel was done as a gift, without any form of compensation involved. It's crucial that the information provided is accurate and truthful to avoid any legal repercussions. Below is a step-by-step guide to help you complete the form accurately.

Once the form is fully completed and duly signed by both parties, it serves as a declaration of the gift, which should then be submitted to the relevant Connecticut state department. This submission is crucial for the official transfer of ownership and the updating of records to reflect the new owner of the vehicle or vessel. Ensuring that all the provided information is accurate and that the form is properly filled out helps streamline this process, making it easier for both the donor and the donee.

What is the Connecticut Au 463 form used for?

The Connecticut Au 463 form, also known as the Motor Vehicle and Vessel Gift Declaration, is used to officially declare that a motor vehicle or vessel has been gifted. It must be filled out when a vehicle or vessel is transferred without any exchange of money, property, or services. The form is required to ensure that the gift transaction is documented and recognized by the state for titling and registration purposes. It also clarifies that there is no outstanding payment or expectation of compensation for the gifted vehicle or vessel.

Who should complete the Au 463 form?

The donor, who is the person gifting the vehicle or vessel, needs to provide their information and affirm that the gift is being given freely without expectation of any compensation or return.

The donee, or the recipient of the gift, must also provide their information and sign the form to acknowledge the receipt of the gift.

Are there any penalties for providing false information on the Au 463 form?

Yes, there are specific penalties for making a false statement on the Au 463 form. As indicated on the form itself, anyone found to have knowingly provided false information can face penalties including imprisonment for up to one year, a fine not exceeding two thousand dollars, or both. It's crucial to thoroughly review and ensure all provided information is accurate and truthful to avoid these penalties.

What information needs to be included on the Au 463 form?

When filling out the Connecticut AU 463 form, also known as the Motor Vehicle and Vessel Gift Declaration, it's important to avoid common mistakes to ensure the process is smooth and the documentation is valid. This form plays a crucial role in the legal transfer of a vehicle or vessel as a gift, without any exchange of money, property, or services. Here are nine mistakes to watch for:

Remember, accurately completing the Connecticut AU 463 form not only ensures compliance with state laws but also provides a clear record of the gift transaction, protecting both the donor's and the donee's interests. Paying close attention to detail and reviewing the form for completeness and accuracy before submission can help avoid delays or legal complications down the line.

When transferring ownership of a motor vehicle or vessel in Connecticut, the AU-463 form plays a pivotal role in declaring the gift transaction between donor and donee. However, this form is often not the only document required in such a transaction. Several other forms and documents usually complement the AU-463 form to ensure a smooth and legally compliant transfer. Each of these documents serves a distinct purpose in the broader context of vehicle or vessel ownership and transfer. Here is a list and brief description of these documents:

Together, these documents facilitate a comprehensive and compliant transfer process when gifting a motor vehicle or vessel in Connecticut. It's imperative for both the donor and donee to be aware of these documents and ensure they are properly completed and submitted along with the AU-463 form. Understanding and utilizing these forms correctly not only helps streamline the transfer but also provides both parties with peace of mind that all legal obligations have been met.

The Connecticut AU-463 form, utilized in the process of gifting a motor vehicle or vessel, bears similarity to several other forms and documents that are used for transferring ownership without traditional sales transactions. These documents facilitate the legal transfer of property while ensuring compliance with specific regulations and taxation laws. Each similar document serves a particular purpose and is tailored for different circumstances or jurisdictions, yet shares common elements with the Connecticut AU-463 form in terms of structure, required information, and legal implications.

1. Affidavit of Motor Vehicle Gift Transfer (Texas Form 14-317)

In terms of purpose and requirements, the Texas Form 14-317, or the Affidavit of Motor Vehicle Gift Transfer, is quite akin to the Connecticut AU-463 form. Both documents are designed for the specific use of recording the gift transfer of a vehicle without financial consideration between the donor and the donee. The similarities include:

2. California DMV Statement of Facts (REG 256)

The California Department of Motor Vehicles' Statement of Facts (REG 256) form shares some key aspects with the Connecticut AU-463 form, despite its broader utility. While the REG 256 can be used for a variety of declarations to the DMV, one of its functions includes the facilitation of vehicle gifts, comparable to what the AU-463 form does. Similarities include:

When filling out the Connecticut AU-463 form, which is crucial for the process of declaring a motor vehicle or vessel as a gift, there are specific steps to ensure the accuracy and legality of the declaration. By adhering to these guidelines, donors and donees can facilitate a smooth transfer of ownership.

Do's:

Don'ts:

Understanding the Connecticut AU-463 form, which is used for declaring the gift of a motor vehicle or vessel, requires clearing up some common misconceptions. Here are ten such misunderstandings:

Addressing these misconceptions is crucial for anyone considering using the AU-463 form to gift a motor vehicle or vessel within Connecticut. It ensures that the process is understood and followed correctly, avoiding any legal complications. By respecting the document's guidelines, donors can properly transfer ownership while adhering to state regulations.

When dealing with the Connecticut AU 463 form, there are several key takeaways to ensure the process is completed accurately and efficiently. This form is used specifically for declaring a motor vehicle or vessel as a gift within Connecticut. Paying attention to the following points can help streamline the process:

Completing the Connecticut AU 463 form accurately is a straightforward process when both parties understand and follow these guidelines. It's a necessary step in the legal transfer of ownership for a motor vehicle or vessel given as a gift, helping to protect all involved parties.

How to Become a Teacher in Connecticut - Instructions for processing the application include submitting a nonrefundable application fee and official transcripts.

Newington Probate Court - It features guidance on how to properly advertise for creditors, a crucial step in ensuring all debts of the estate are known and addressed.

Har 3 Connecticut - It includes a section that must be filled out by healthcare providers, including details from a physical exam and assessments of various health aspects.