Fill Out a Valid Connecticut Au 738 Template

Fill Out a Valid Connecticut Au 738 Template

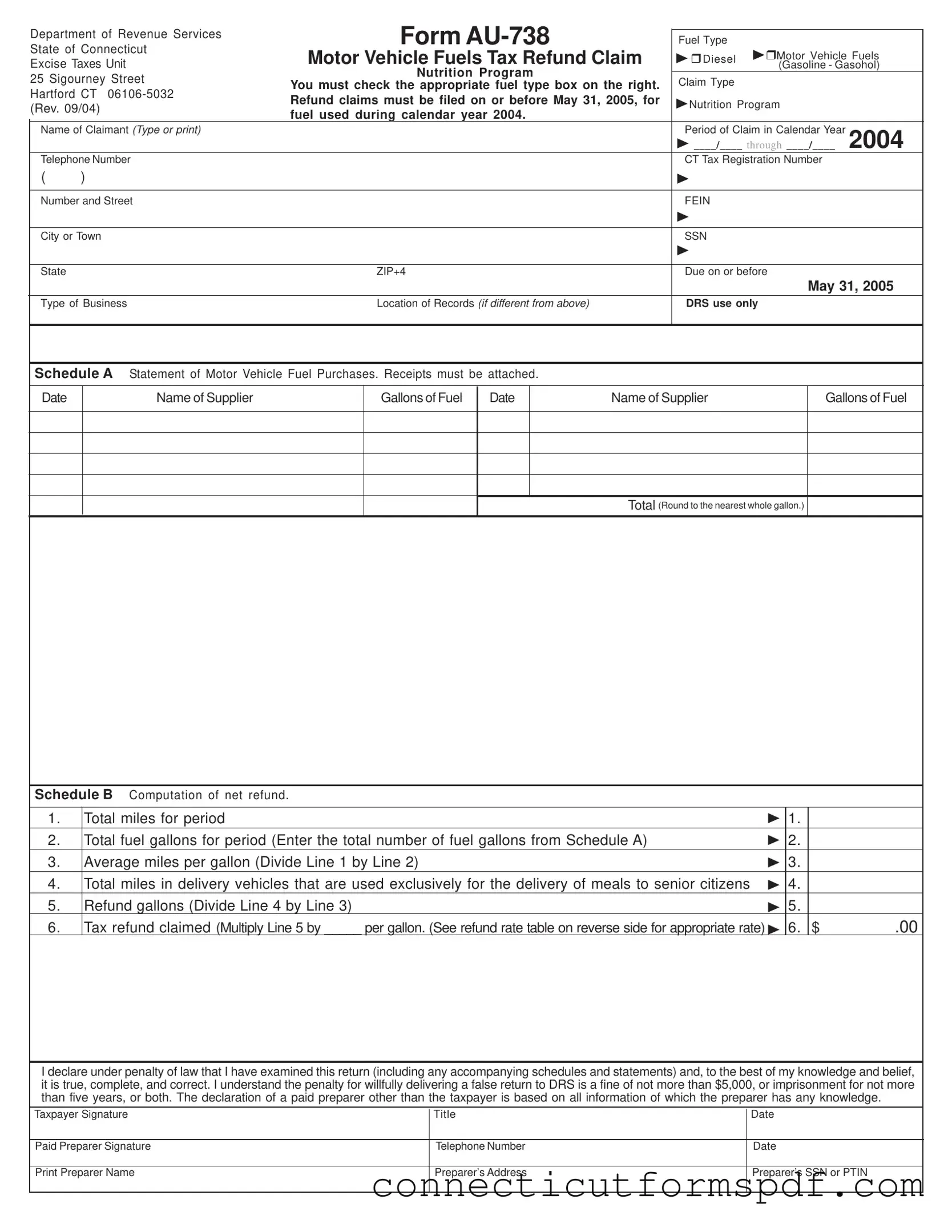

The Connecticut Department of Revenue Services Form AU-738 presents a structured procedure for entities to claim a motor vehicle fuels tax refund, specifically for fuel used in calendar year 2024. This form is meticulously designed to accommodate claims for diesel, gasoline, and gasohol under the umbrella of excise taxes, with a special focus on the Nutrition Program. It mandates claimants to select the appropriate fuel type and provide exhaustive details such as the period of claim within the specified calendar year, alongside personal and business information. Essential to the process are Schedule A and B, requiring detailed documentation of fuel purchases and a precise computation of the net refund, respectively. This computation involves calculations based on total miles covered, fuel efficiency, and dedicated miles for delivering meals to senior citizens, aiming to ensure accuracy and fairness in the refund process. Furthermore, the form underscores the importance of adherence to deadlines, with a clear cut-off date for submissions, and establishes the linkage between the claimant and the Department by requesting contact information and a Connecticut tax registration number or Social Security Number. Detailed instructions guide the claimant through requirements for supporting documents and the conditions under which the refund is calculated and claimed, emphasizing the legal obligations and the consequences of falsification. Additionally, it addresses the retention of records, rounding off procedures for financial figures, and the necessity of including a contract with the local area agency on aging as proof of eligibility. The resolution process for any errors or disputes involves direct communication with the Excise Taxes Unit, providing a clear path for inquiries or additional assistance.

Department of Revenue Services |

|

Form |

|

Fuel Type |

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|||

State of Connecticut |

Motor Vehicle Fuels Tax Refund Claim |

Diesel |

(Gasoline - Gasohol) |

|||||||||

Excise Taxes Unit |

||||||||||||

|

|

|

|

|

|

|

|

|

Motor Vehicle Fuels |

|||

25 Sigourney Street |

|

Nutrition Program |

|

|

|

|

|

|

||||

|

|

Claim Type |

|

|

|

|

||||||

You must check the appropriate fuel type box on the right. |

|

|

|

|

||||||||

Hartford CT |

|

|

|

|

||||||||

Refund claims must be filed on or before May 31, 2005, for |

Nutrition Program |

|

||||||||||

(Rev. 09/04) |

|

|||||||||||

fuel used during calendar year 2004. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

||||

Name of Claimant (Type or print) |

|

|

|

|

|

Period of Claim in Calendar Year |

2004 |

|||||

|

|

|

|

|

|

|

|

____/____ through ____/____ |

||||

Telephone Number |

|

|

|

|

|

CT Tax Registration Number |

|

|||||

( |

) |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Number and Street |

|

|

|

|

|

FEIN |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City or Town |

|

|

|

|

|

SSN |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

State |

|

|

|

ZIP+4 |

|

|

|

Due on or before |

|

|||

|

|

|

|

|

|

|

|

|

|

|

May 31, 2005 |

|

Type of Business |

|

Location of Records (if different from above) |

|

DRS use only |

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

Schedule A Statement of Motor Vehicle Fuel Purchases. Receipts must be attached. |

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

Date |

|

Name of Supplier |

|

Gallons of Fuel |

Date |

|

Name of Supplier |

|

|

Gallons of Fuel |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total (Round to the nearest whole gallon.) |

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule B Computation of net refund. |

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

||

1. |

Total miles for period |

|

|

|

|

|

|

1. |

|

|

||

2. |

Total fuel gallons for period (Enter the total number of fuel gallons from Schedule A) |

|

2. |

|

|

|||||||

3. |

Average miles per gallon (Divide Line 1 by Line 2) |

|

|

|

|

3. |

|

|

||||

4. |

Total miles in delivery vehicles that are used exclusively for the delivery of meals to senior citizens |

4. |

|

|

||||||||

5. |

Refund gallons (Divide Line 4 by Line 3) |

|

|

|

|

5. |

|

|

||||

6. |

|

Tax refund claimed (Multiply Line 5 by _____ per gallon. (See refund rate table on reverse side for appropriate rate) |

6. |

$ |

.00 |

|||||||

I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return to DRS is a fine of not more than $5,000, or imprisonment for not more than five years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Taxpayer Signature |

Title |

Date |

|

|

|

Paid Preparer Signature |

Telephone Number |

Date |

|

|

|

Print Preparer Name |

Preparer’s Address |

Preparer’s SSN or PTIN |

|

|

|

Instructions

Your motor vehicle fuels tax refund claim for fuel used during calendar year 2004 must:

1.Be filed with Department of Revenue Services (DRS) on or before May 31, 2005; and

2.Involve at least 200 gallons of fuel eligible for tax refund.

The appropriate fuel type box must be marked on the front of this form in order to process this claim. You must file a separate Form

Be sure to provide a telephone number where you can be contacted.

You must indicate your Connecticut tax registration number or Social Security Number in the space provided.

For all purchases of fuel listed, you must attach a copy of each numbered slip or invoice issued at the time of the purchase. The slip or invoice may be the original or a photocopy and must show the:

•Date of purchase;

•Name and address of the seller (which must be printed or rubber stamped on the slip or invoice);

•Name and address of the purchaser (which must be the name and address of the person or entity filing the claim for refund);

•Number of gallons of fuel purchased;

•Price per gallon;

•Total amount paid; and

•If payment is made within a discounted period, provide proof of amount paid.

You must retain records to substantiate your refund claim for at least three years following the filing of the claim and make them

Table of Motor Vehicle Fuels Tax Refund Rates for 2004

for Nutrition Program

Diesel January 1, 2004 |

through |

December 31, 2004 |

26¢ |

per Gallon |

Motor Vehicle Fuels |

|

|

|

|

January 1, 2004 |

through |

December 31, 2004 |

25¢ |

per Gallon |

Note: You must file a separate Form

available to DRS upon request.

Rounding Off to Whole Dollars: You must round off cents to the nearest whole dollar on your motor vehicle fuels tax refund claim. Round down to the next lowest dollar all amounts that include 1 through 49 cents. Round up to the next highest dollar all amounts that include 50 through 99 cents. However, if you need to add two or more amounts to compute the total to enter on a line, include cents and round off only the total.

Example: Add two amounts ($1.29 + $3.21) to compute the total ($4.50) to enter on a line. $4.50 is rounded to $5.00 and entered on the line.

You must attach a copy of your contract with your local area agency on aging as evidence of your eligibility to provide Title

Mail the completed refund application to: Department of Revenue Services State of Connecticut

Excise Taxes Unit

25 Sigourney Street Hartford CT

Additional Information

If you need additional information or assistance, please call the Excise Taxes Unit at

www.ct.gov/DRS

Your refund will be applied against any outstanding DRS tax liability.

Form

| Fact | Detail |

|---|---|

| 1. Form Type | Connecticut AU 738 Motor Vehicle Fuels Tax Refund Claim |

| 2. Governing Body | Department of Revenue Services, State of Connecticut |

| 3. Eligible Fuel Types | Diesel, Gasoline, Gasohol |

| 4. Purpose | Refund Claim for Motor Vehicle Fuels Tax for Nutrition Program |

| 5. Deadline for Filing | On or before May 31, 2005, for fuel used during calendar year 2004 |

| 6. Documentation Required | Receipts for all purchases, completed schedules A and B, proof of contract with local area agency on aging |

| 7. Governing Laws | State of Connecticut Motor Vehicle Fuels Tax legislation |

Filing the Connecticut AU-738 form is a straightforward process once you have all the necessary information on hand. This form is designed for businesses to claim a motor vehicle fuels tax refund for fuel used in certain activities, such as delivering meals to senior citizens. Close attention to detail and ensuring all required documentation is attached is crucial for a successful claim.

After submitting your form AU-738, it's important to maintain copies of your filed claim and all supporting documentation for at least three years. This documentation may be requested by the Department of Revenue Services for verification purposes. Should you have any questions or require further assistance, the Excise Taxes Unit is available to help during business hours. Remember, timely and accurate filing ensures a smoother process for claiming your tax refund.

Frequently Asked Questions about the Connecticut AU-738 Form

Form AU-738 is used to claim a refund for motor vehicle fuels taxes paid in the state of Connecticut. It is specifically for fuel (diesel, gasoline, or gasohol) used in calendar year 2004 and is applicable for certain programs, such as nutrition programs delivering meals to senior citizens. This form allows entities to recoup some of the funds spent on fuel used for eligible activities.

Any individual or business entity that has purchased motor vehicle fuel for use in a qualified operation, such as delivery vehicles for nutrition programs targeting senior citizens, must file Form AU-738 to claim their tax refund. It is essential that the claimant has a Connecticut tax registration number or Social Security Number to file this form.

To successfully process a refund claim using Form AU-738, the claimant needs to attach a copy of each purchase slip or invoice for the fuel. These documents need to detail the date of purchase, the seller and purchaser's name and address, number of gallons purchased, price per gallon, and the total amount paid. Additionally, evidence of a contract with a local area agency on aging must be provided to substantiate eligibility for filing under the nutrition program clause.

The deadline to file Form AU-738 is on or before May 31, 2005, for fuel used during the calendar year 2004. It is crucial to adhere to this deadline to ensure eligibility for the tax refund.

The refund on Form AU-738 is calculated by first determining the total miles driven by delivery vehicles exclusively used for delivering meals to senior citizens, and then dividing this number by the average miles per gallon to find the refundable gallons. The refundable amount in dollars is then calculated by multiplying the refundable gallons by the tax rate per gallon (either 26¢ for diesel or 25¢ for motor vehicle fuels in 2004).

After submitting Form AU-738, the Department of Revenue Services (DRS) in Connecticut processes the refund claim. The claimant must ensure all information provided is accurate and complete to avoid any delays. If approved, the refund will be applied against any outstanding tax liabilities with DRS. For additional information or assistance, claimants can contact the Excise Taxes Unit directly.

When completing the Connecticut AU-738 form for Motor Vehicle Fuels Tax Refund claims, several common errors can occur. These mistakes can delay the processing of a refund or potentially result in a refused claim. Understanding these pitfalls is the first step towards ensuring your refund claim is successful.

One of the first mistakes made is not selecting the correct fuel type at the beginning of the form. This form allows for the refund claim of diesel, gasoline, or gasohol. Accurately marking the appropriate box is crucial since different fuel types have distinct tax refund rates, and failure to do so can invalidate the claim.

Another common error involves the Schedule A Statement of Motor Vehicle Fuel Purchases. All fuel purchases must be accompanied by a corresponding receipt or invoice. However, claimants often submit the form without attaching these crucial documents. The receipts or invoices validate the amount of fuel purchased and are essential for processing the refund. Each document must clearly show the date of purchase, the seller’s and purchaser’s name and address, the number of gallons purchased, the price per gallon, and the total amount paid.

Lastly, failing to sign and date the form is a common but critical error. The form bears a declaration that must be signed by the taxpayer, attesting to the accuracy and completeness of the information provided. An unsigned form is considered incomplete and cannot be processed. Equally important is the requirement for proof of a contract with a local area agency on aging as evidence of eligibility to provide Title III-C meals to senior citizens, which is frequently overlooked.

In conclusion, to ensure a smooth refund process, it is imperative to attend to the details required on the Connecticut AU-738 form. From accurately indicating the fuel type to attaching all necessary documentation and correctly rounding figures, each step is crucial. Awareness and avoidance of these common errors can help facilitate a timely and successful refund claim.

When handling Connecticut's Form AU-738, a fuel tax refund claim for motor vehicle fuels like diesel and gasoline, individuals and businesses enter the complex terrain of tax documentation, requiring a clear roadmap for navigation. Beyond the AU-738, there's a suite of forms and documents often needed to ensure the journey leads to a successful claim. Each document plays a unique role, acting as a cog in the larger machinery of tax compliance and refund processing. Here's a closer look at these essential components:

The journey through tax documentation, particularly for specific claims like those facilitated by Form AU-738, requires careful attention to detail and thorough preparation. Understanding the role of each form and document in this process is paramount. With the right documentation in hand, individuals and businesses can navigate the complexities of tax refunds with greater confidence and efficiency, ultimately ensuring that they fulfill all requirements for a successful claim.

The Connecticut AU-738 form is similar to the Federal Form 8849 (Schedule 1), which is used for claiming refunds on federal excise taxes for fuels. Both forms require the claimant to specify the type of fuel for which the refund is being requested and to document the quantity of fuel purchased. They also necessitate detailed calculations to determine the eligible refund amount based on the fuel used during a specified period. Additionally, claimants must attach supporting documents, such as purchase receipts or invoices, that validate the amount of fuel bought and used.

Another document similar to the Connecticut AU-738 form is the IRS Form 4136, Credit for Federal Tax Paid on Fuels. Like the AU-738, Form 4136 is utilized to claim a credit or refund for the tax on fuel that was used for certain purposes eligible under the law. Both forms necessitate the claimant to provide detailed information about the type and amount of fuel used, and they require supporting documentation to substantiate the claim. However, Form 4136 is specifically used when claimants are looking to claim credits on their federal income tax return, while the AU-738 is for direct refunds from the state for fuels taxes paid.

When preparing to fill out the Connecticut AU-738 form for a motor vehicle fuels tax refund claim, there are several important dos and don'ts to keep in mind to ensure the process is smooth and the application is successful.

Do:Understanding the Connecticut Department of Revenue Services Form AU-738 can be challenging, with several misconceptions surrounding its purpose, requirements, and filing process. Below are nine common misconceptions about this form, clarified to assist in accurately navigating the refund claim process.

It's only for gasoline purchases. This is incorrect. The AU-738 form is for claims related to diesel, gasoline, and gasohol used within specific programs, including the Nutrition Program for senior citizens.

The form covers fuel used at any time. Actually, the form is specifically for fuel utilized during the 2004 calendar year, with claims needing to be filed by May 31, 2005.

Any amount of fuel is claimable. Not quite. Eligibility for a refund requires the use of at least 200 gallons of motor vehicle fuel.

Information can be submitted without receipts. On the contrary, claimants must attach a copy of the numbered slip or invoice for all fuel purchases, providing detailed purchase information.

The form doesn't require substantiation of claims. In fact, claimants must retain records of fuel purchases and use for at least three years after filing and present them to the Department of Revenue Services upon request.

You don't need to specify the fuel type. Incorrectly assumed, claimants must mark the appropriate fuel type box on the form to process the claim for a specific fuel type.

A single form can cover multiple fuel types. This is mistaken. Separate forms must be filed for each type of motor vehicle fuel for which a refund is claimed.

The claimed amount doesn't need to be rounded. Actually, the form instructs to round off cents to the nearest whole dollar on your motor vehicle fuels tax refund claim, following specific rounding instructions.

The refund is automatically granted upon submission. Not exactly, the refund will first be applied against any outstanding tax liabilities with the DRS, and additional validation steps may be required.

Understanding the correct procedures and requirements for filing Form AU-738 ensures that eligible claimants successfully navigate the refund claim process, avoiding common pitfalls and mistakes. When in doubt, reaching out to the Excise Taxes Unit for assistance or visiting the DRS website for more information can provide clarity and support.

Filling out and using the Connecticut AU-738 form involves a process that is designed to help eligible claimants receive a tax refund for motor vehicle fuel. To streamline this process and ensure a successful claim, here are six key take.mapbox.com from the specifics of the form:

Understanding these key elements is essential for successfully navigating the refund claim process with the Connecticut AU-738 form. Proper attention to detail, from adhering to deadlines to maintaining thorough purchase records, can significantly impact the outcome of a refund claim.

How to Transfer Ownership of a Car to a Family Member in Ct - The form serves as a notification to the Connecticut DMV, streamlining the process of managing abandoned vehicles.

Ct Dmv License Restoration - Compliance with this bond requirement is crucial for maintaining licensure for operating a vehicle-related business within Connecticut.