Fill Out a Valid Connecticut Op 300 Template

Fill Out a Valid Connecticut Op 300 Template

In the dynamic landscape of Connecticut's regulatory environment, one document stands as a cornerstone for businesses involved with tobacco products: the Department of Revenue Services Form OP-300. This form, crucial for ensuring compliance with state tax protocols, serves a pivotal role for distributors, whether they deal in cigars, snuff, or other types of tobacco. The essence of the form lies in its detailed approach to tracking the flow of tobacco products within, into, and out of Connecticut, requiring registrants to accurately report quantities and types of products to calculate the taxes due meticulously. From specifying categories of tobacco excluded from certain taxes to delineating the process for reporting untaxed roll-your-own cigarette tobacco, the OP-300 encapsulates a spectrum of activities essential for accurate tax submission. Moreover, it accommodates scenarios like business closure or amendment of previously submitted returns, underscoring the state's adaptability to business realities. The form also outlines penalties for non-compliance, emphasizing the gravity of accurate reporting and timely tax payment. Designed to be user-friendly, it offers a methodical structure for reporting, supported by a suite of schedular attachments that encapsulate various categories of tobacco products, thereby streamlining the tax filing process. Additionally, the OP-300 form fosters a digital-first approach, encouraging electronic payments to expedite processing and ensure timely compliance, reflecting modern administrative efficiencies. As such, the form not only lays the groundwork for tax compliance but also encapsulates the state's commitment to leveraging structured data collection in safeguarding public interests and ensuring the fiscal responsibilities of tobacco distributors are met with precision.

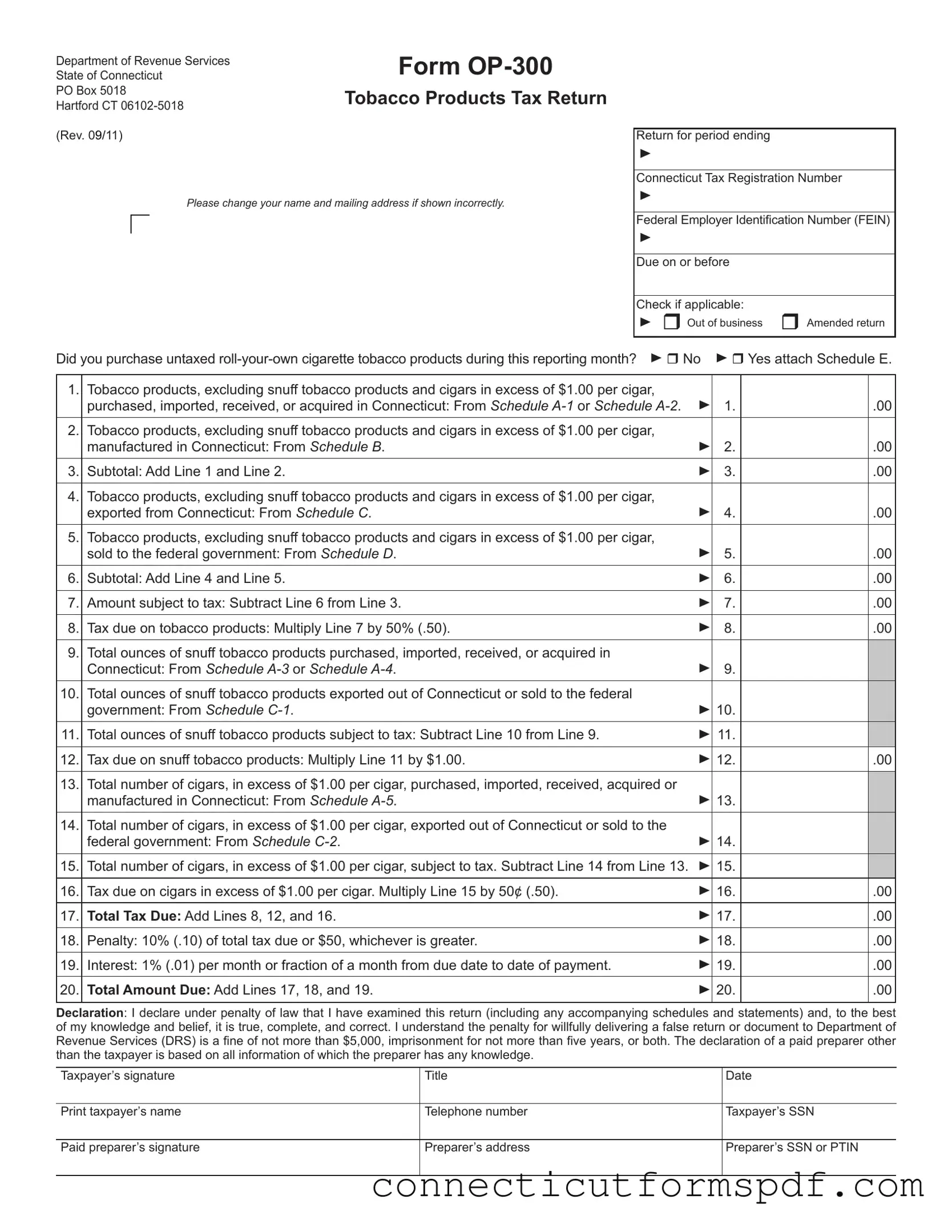

Department of Revenue Services |

Form |

|

State of Connecticut |

||

PO Box 5018 |

Tobacco Products Tax Return |

|

Hartford CT |

||

|

||

(Rev. 09/11) |

|

Please change your name and mailing address if shown incorrectly.

Return for period ending

Connecticut Tax Registration Number

Federal Employer Identiication Number (FEIN)

Due on or before

Check if applicable:

Out of business Amended return

Did you purchase untaxed

1. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

purchased, imported, received, or acquired in Connecticut: From Schedule |

|

1. |

|

.00 |

|

|

|

|

|

|

2. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

manufactured in Connecticut: From Schedule B. |

|

2. |

|

.00 |

|

|

|

|

|

|

3. |

Subtotal: Add Line 1 and Line 2. |

|

3. |

|

.00 |

|

|

|

|

|

|

4. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

exported from Connecticut: From Schedule C. |

|

4. |

|

.00 |

|

|

|

|

|

|

5. |

Tobacco products, excluding snuff tobacco products and cigars in excess of $1.00 per cigar, |

|

|

|

|

|

sold to the federal government: From Schedule D. |

|

5. |

|

.00 |

|

|

|

|

|

|

6. |

Subtotal: Add Line 4 and Line 5. |

|

6. |

|

.00 |

|

|

|

|

|

|

7. |

Amount subject to tax: Subtract Line 6 from Line 3. |

|

7. |

|

.00 |

|

|

|

|

|

|

8. |

Tax due on tobacco products: Multiply Line 7 by 50% (.50). |

|

8. |

|

.00 |

|

|

|

|

|

|

9. |

Total ounces of snuff tobacco products purchased, imported, received, or acquired in |

|

|

|

|

|

Connecticut: From Schedule |

|

9. |

|

|

10. |

Total ounces of snuff tobacco products exported out of Connecticut or sold to the federal |

|

|

|

|

|

government: From Schedule |

|

10. |

|

|

11. |

Total ounces of snuff tobacco products subject to tax: Subtract Line 10 from Line 9. |

|

11. |

|

|

12. |

Tax due on snuff tobacco products: Multiply Line 11 by $1.00. |

|

12. |

|

.00 |

|

|

|

|

|

|

13. |

Total number of cigars, in excess of $1.00 per cigar, purchased, imported, received, acquired or |

|

|

|

|

|

manufactured in Connecticut: From Schedule |

|

13. |

|

|

14. |

Total number of cigars, in excess of $1.00 per cigar, exported out of Connecticut or sold to the |

|

|

|

|

|

federal government: From Schedule |

|

14. |

|

|

15. |

Total number of cigars, in excess of $1.00 per cigar, subject to tax. Subtract Line 14 from Line 13. |

|

15. |

|

|

16. |

Tax due on cigars in excess of $1.00 per cigar. Multiply Line 15 by 50¢ (.50). |

|

16. |

|

.00 |

17. |

Total Tax Due: Add Lines 8, 12, and 16. |

|

17. |

|

.00 |

|

|

|

|

|

|

18. |

Penalty: 10% (.10) of total tax due or $50, whichever is greater. |

|

18. |

|

.00 |

|

|

|

|

|

|

19. |

Interest: 1% (.01) per month or fraction of a month from due date to date of payment. |

|

19. |

|

.00 |

|

|

|

|

|

|

20. |

Total Amount Due: Add Lines 17, 18, and 19. |

|

20. |

|

.00 |

|

|

|

|

|

|

Declaration: I declare under penalty of law that I have examined this return (including any accompanying schedules and statements) and, to the best of my knowledge and belief, it is true, complete, and correct. I understand the penalty for willfully delivering a false return or document to Department of

Revenue Services (DRS) is a ine of not more than $5,000, imprisonment for not more than ive years, or both. The declaration of a paid preparer other than the taxpayer is based on all information of which the preparer has any knowledge.

Taxpayer’s signature |

Title |

Date |

Print taxpayer’s name

Telephone number

Taxpayer’s SSN

Paid preparer’s signature

Preparer’s address

Preparer’s SSN or PTIN

General Instructions

Complete the return in blue or black ink only.

Taxpayers must ile a return for each calendar month by the

Example: The tobacco products tax return for January 1 through

January 31 must be iled on or before February 25.

Taxpayers must ile a return even if no tax is due. All

supporting schedules can be found on the Department of Revenue Services (DRS) website at www.ct.gov/DRS

The owner, a partner, or a principal oficer must sign this

return.

Pay Electronically: Visit www.ct.gov/TSC to use the Taxpayer Service Center (TSC) to make a direct tax

payment. After logging onto the TSC, select the Make Payment Only option and choose a tax type from the drop down box. Using this option authorizes the DRS to electronically withdraw from your bank account (checking or savings) a payment on a date you select up to the due date.

As a reminder, even if you pay electronically you must still ile your return by the due date. Tax not paid on or before the

due date will be subject to penalty and interest.

If you do not pay electronically, make check payable to Commissioner of Revenue Services. DRS may submit

your check to your bank electronically.

Mail to: Department of Revenue Services

State of Connecticut

PO Box 5018

Hartford CT

Deinitions

TOBACCO PRODUCTS means: Cigars, cheroots, stogies, periques, granulated, plug cut, crimp cut, ready rubbed and

other smoking tobacco, cavendish, plug and twist tobacco, ine cut and other chewing tobaccos, shorts, refuse scraps,

clippings, cuttings and sweepings of tobacco, and all other kinds and forms of tobacco prepared in a manner as to be suitable for chewing or smoking in a pipe or otherwise for both

chewing and smoking, but does not include any cigarettes as deined in Conn. Gen. Stat.

SNUFF TOBACCO PRODUCTS means: Tobacco products that have imprinted on the packages the designation “snuff” or

“snuff lour” or the federal tax designation “Tax Class M,” or

both.

WHOLESALE SALES PRICE means:

•In the case of a distributor that is the manufacturer of the tobacco products, the price set for these products or, if no price has been set, the wholesale value of these products.

•In the case of a distributor that is not the manufacturer of the tobacco products, the price at which the distributor purchased the products.

Speciic Instructions

Check Box: You must check the appropriate box concerning the purchase of untaxed

Line 1

Resident Distributor: Enter from Schedule

wholesale sales price of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar)

purchased, imported, received, or acquired in Connecticut by the distributor.

Nonresident Distributor: Enter from Schedule

tobacco products and cigars in excess of $1.00 per cigar)

imported into Connecticut by the distributor.

Line 2 - Enter from Schedule B the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) manufactured in

Connecticut by the distributor.

Line 4 - Enter from Schedule C the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) exported from Connecticut

that were imported, received, purchased, acquired, or manufactured in Connecticut by the distributor. Prepare a separate Schedule C for each state of destination. (Use Line 9 and Line 10 to report snuff products and Line 13 and

Line 14 to report cigars in excess of $1.00 per cigar.)

Line 5 - Enter from Schedule D the wholesale sales price

of tobacco products (excluding snuff tobacco products and cigars in excess of $1.00 per cigar) sold to the federal

government that were imported, received, purchased, acquired, or manufactured in Connecticut by the distributor.

Line 9 - Enter from Schedule

Line 10 - Enter from Schedule

Line 13 - Enter from Schedule

acquired, or manufactured in Connecticut.

Line 14 - Enter from Schedule

sold to the federal government.

For Further Information

If you need additional information or assistance, please call the Excise Taxes Unit at

Forms and Publications: Visit the DRS website at www.ct.gov/DRS to download and print Connecticut tax

forms and publications.

TTY, TDD, and Text Telephone users only may transmit inquiries anytime by calling

| Fact | Detail |

|---|---|

| Form Title | Connecticut Department of Revenue Services Form OP-300, Tobacco Products Tax Return |

| Revision Date | September 2011 (Rev. 09/11) |

| Filing Requirement | Taxpayers must file a return for each calendar month by the twenty-fifth day of the following month. |

| Electronic Filing | Taxpayers can use the Taxpayer Service Center (TSC) to make direct tax payments electronically and must file their return by the due date, even if paying electronically. |

| Penalties | Penalty for late payment: 10% (.10) of total tax due or $50, whichever is greater, plus interest at 1% (.01) per month from due date to date of payment. |

| Tax Calculation | The tax is calculated for different categories of tobacco: a 50% (.50) tax rate on certain tobacco products, a $1.00 tax for snuff tobacco products, and a 50¢ (.50) tax for cigars in excess of $1.00 per cigar. |

| Governing Law | Connecticut General Statutes §12-285 defines cigarettes and outlines tobacco product regulations, including taxation. |

After you’ve gathered all necessary documentation and information regarding your tobacco product transactions within the reporting period, filling out the Connecticut OP-300 form is the next step in complying with state tax regulations. It is mandatory for businesses involved in the distribution of tobacco products within Connecticut to submit this form accurately and on time. The process involves detailing your transactions to calculate and report the taxes due on tobacco products, snuff, and cigars, ensuring all such products are taxed according to Connecticut law. This form also provides an opportunity to declare any untaxed roll-your-own tobacco products purchased during the reporting period. It is crucial for the accuracy of your tax submissions and to avoid any penalties or interest for late or incorrect filings.

Once you have completed and double-checked the form for accuracy, submit it along with any payment due to the specified address by the due date to avoid penalties. Remember, even if no tax is due for the reporting period, submission of the form is still required. This obligation ensures compliance with Connecticut's tax laws regarding tobacco products, securing lawful operations within the state.

What is the Connecticut OP-300 Form?

The Connecticut OP-300 Form is a Tobacco Products Tax Return required by the Department of Revenue Services. Businesses involved in the purchase, importation, reception, or acquisition of tobacco products in Connecticut must complete this form. It encompasses various types of tobacco products excluding snuff and premium cigars over $1.00 per item. This form helps in reporting and calculating the taxes due for tobacco products within the state.

Who needs to file the OP-300 Form?

Any distributor of tobacco products in Connecticut, whether a resident or non-resident distributor, needs to file the OP-300 Form. This includes entities that manufacture tobacco products in the state or those who import, receive, purchase, or acquire tobacco products for sale within the state. It is also required if untaxed roll-your-own cigarette tobacco products have been purchased during the reporting month.

When is the OP-300 Form due?

The OP-300 Form is due on or before the twenty-fifth day of the month following the reporting month. For instance, the tax return covering the period of January 1st through January 31st is due by February 25th. Timely submission is crucial to avoid penalties and interest charges for late filings.

How can the tax due on the OP-300 Form be calculated?

Tax due on tobacco products is calculated differently based on the type of product. For tobacco products excluding snuff and cigars priced over $1.00, the tax is 50% of the product's wholesale sales price. Snuff tobacco products are taxed at $1.00 per ounce, and cigars costing more than $1.00 are taxed at 50 cents each. The form includes detailed sections for calculating the subtotal of taxable products and determining the total tax due by incorporating various adjustments for sales, exports, and government sales.

What payment methods are available for the OP-300 Form?

Filers have the option to pay electronically via the Taxpayer Service Center (TSC) on the Connecticut Department of Revenue Services website. This platform allows for direct payment from a bank account by selecting the tax type and due date for the payment. If not paying electronically, checks made payable to the Commissioner of Revenue Services are accepted. All payments should be sent to the Department of Revenue Services at the designated P.O. Box in Hartford, CT. Remember, even if paying electronically, the return must still be filed by the due date to avoid penalties and interest.

Filling out the Connecticut Department of Revenue Services Form OP-300, the Tobacco Products Tax Return, can be a challenging task fraught with the potential for errors. Given the complexity and the nuanced requirements of this tax form, there are common mistakes to look out for when completing it.

One of the initial and most fundamental mistakes is incorrect or outdated personal and business information. Taxpayers often fail to update their name and mailing address, although the form explicitly provides an opportunity to do so. This oversight can lead to misdirected correspondence or legal notices that may have critical tax implications.

In the area of product reporting, a frequent error involves improperly categorizing tobacco products. The form divides tobacco products into several categories, such as snuff and cigars exceeding $1.00 per cigar, with different tax rates applied to each. Misclassification can lead to incorrect tax calculations, underpayments, or overpayments. Proper classification requires careful attention to the definitions provided by the form and may necessitate additional documentation or clarification.

The form distinctively separates tobacco products into items subject to tax and those that are not, such as exports or sales to the federal government. A common mistake includes inaccurately reporting exported tobacco products or those sold to the federal government, which can cause an inflated tax obligation. Detailing these amounts requires precision and an understanding of the exemption criteria.

To avoid these errors, thorough reading, meticulous preparation, and attention to detail are essential. In addition, staying informed about changes to tax laws and rates as they pertain to tobacco products in Connecticut can help ensure the accuracy and timeliness of your Form OP-300 submissions.

In managing tobacco product sales and distributions, businesses in Connecticut must go beyond submitting the OP-300 form by incorporating additional forms and documents to ensure compliance and accurate tax reporting. These complementing documents span from detailed schedules to forms that validate exemptions or corrections, each playing an essential role in the tax filing process.

Collectively, these documents facilitate a comprehensive approach to tax reporting for tobacco products in Connecticut. Businesses must meticulously prepare and submit the correct supplementary documents along with the OP-300 form, ensuring their tax responsibilities are met in full compliance with state regulations. Understanding the purpose and requirements of each form enhances the accuracy of tax filings and minimizes the risk of penalties for underreported taxes or non-compliance.

The Connecticut Op 300 form is similar to other forms used for tax reporting and compliance, but it has its own unique focus on tobacco products. This form is a prime example of how specific industries are monitored and taxed, ensuring that distributors comply with state regulations. Its structure and purpose draw parallels to several other tax forms, each tailored to particular goods or services.

Form TTB F 5000.24, the Federal Excise Tax Return used by the Alcohol and Tobacco Tax and Trade Bureau (TTB), is a document that bears resemblance to the Connecticut Op 300 form. Both forms are designed for the reporting and paying of excise taxes—however, they operate at different government levels and for slightly varied purposes. The Federal Excise Tax Return is broader, covering alcohol, tobacco, firearms, and ammunition. Meanwhile, the Op 300 hones in specifically on tobacco products within Connecticut. Each form requires detailed accounting of products manufactured, imported, or sold, but the TTB F 5000.24 encompasses a wider spectrum of taxable goods beyond just tobacco.

Form MT-203, New York's Cigarette and Tobacco Products Tax Return, is another document with similarities to Connecticut’s Op 300. Like the Op 300, the MT-203 targets tobacco products, focusing on the reporting and tax obligations at the state level. These forms share a common goal: to collect taxes on tobacco sales and distribution within their respective states. The specifics, such as tax rates and exemptions, may differ between New York and Connecticut, but the overarching structure remains consistent. Both necessitate detailed tracking and reporting of tobacco products to ensure the correct taxes are paid.

In essence, while the Connecticut Op 300 form is unique to its state and specific to tobacco products, it shares commonalities with various other excise tax forms across the country. Its parallels with forms like the TTB F 5000.24 and New York's MT-203 illuminate the broader framework of excise tax reporting in the United States. Each form, whether federal or state, plays a crucial role in the regulation and taxation of commodities such as tobacco, providing a means to monitor and collect revenue necessary for public services.

When dealing with the Connecticut OP-300 form, which is a crucial document for reporting and paying taxes on tobacco products, it's essential to proceed with care and accuracy. Here are 10 do's and don'ts that will guide you through the process smoothly.

Do:

Don't:

Adhering to these suggested practices when completing the Connecticut OP-300 form will not only ensure compliance with the state's tax laws but also protect against possible legal and financial repercussions.

Understanding the Connecticut OP-300 form involves navigating through a fair amount of complexity. However, several misconceptions commonly arise about this form, affecting compliance and accuracy in tobacco products taxation. Here are seven widespread myths and the truths that dispel them:

Dispelling these misconceptions is critical for accurate tax compliance and reporting. Taxpayers dealing with tobacco products in Connecticut should familiarize themselves with the specifics of the OP-300 form to ensure they meet all requirements and avoid potential penalties associated with misinformation.

Filling out and using the Connecticut OP-300 form, known as the Tobacco Products Tax Return, is a necessary task for businesses handling tobacco products within the state. To ensure compliance and avoid common pitfalls, here are key takeaways:

Remember, the declaration at the end of the form is a legal document. Falsely filing it can lead to severe penalties, including fines and imprisonment. Always review your information carefully and consult with a professional if you're unsure about any part of the process.

Har 3 Connecticut - Immunization records are a critical part of this form, with specific requirements for school entry and additional booster shots detailed for compliance.

Ct License Renewal Fee - The application process includes legal attestations to the truthfulness of provided information, ensuring integrity.

Connecticut Realtors - Stipulates the handover protocol, including the property's condition and the exact timing of possession by the buyer.