Fill Out a Valid Connecticut Sba 2 Template

Fill Out a Valid Connecticut Sba 2 Template

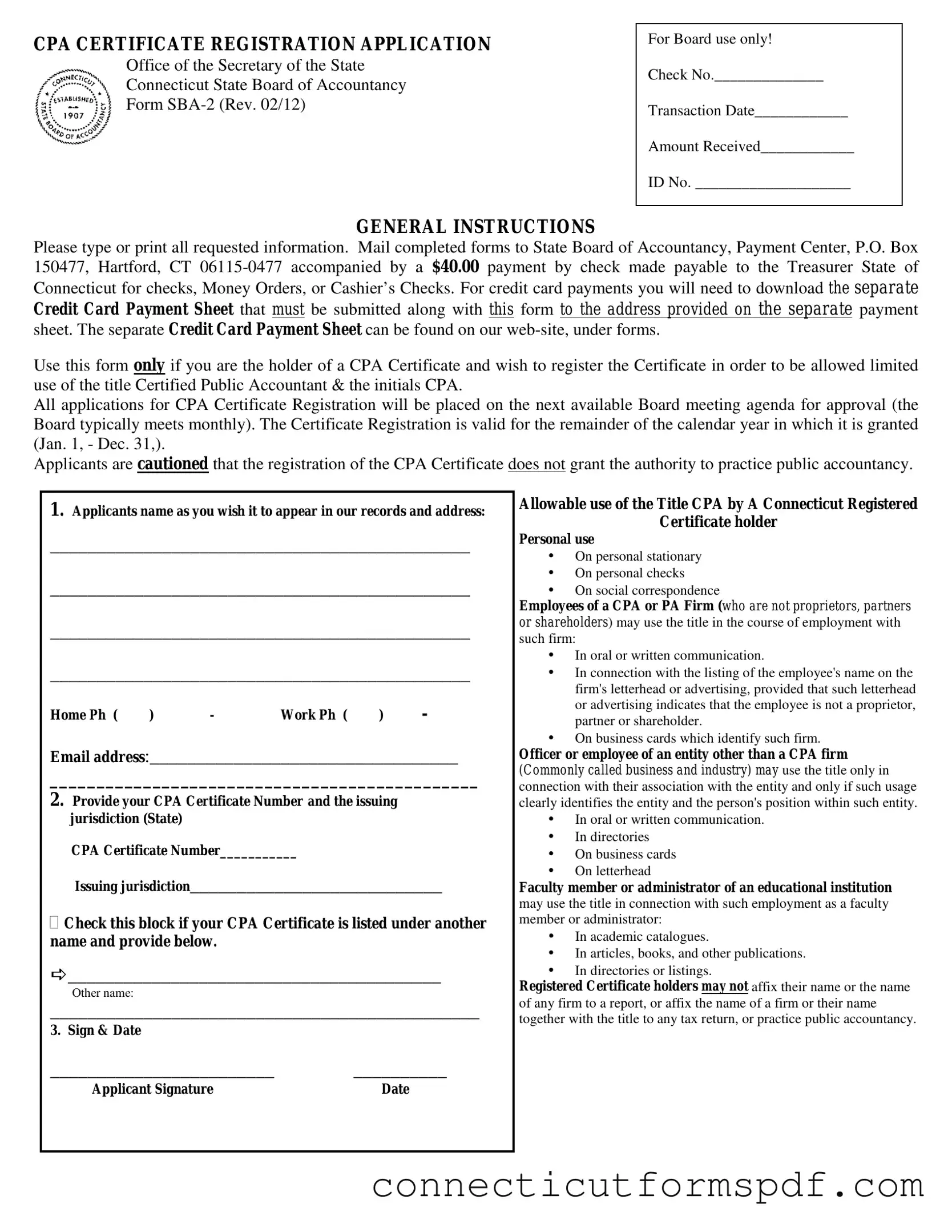

Navigating the procedures for registering a CPA certificate in Connecticut is made clearer with the Connecticut SBA-2 form, a vital document for Certified Public Accountants within the state. This form, revised in February 2012 and issued by the Connecticut State Board of Accountancy under the Office of the Secretary of the State, serves a specific purpose: it allows holders of CPA certificates to register their titles for limited use within the state. The form outlines the general instructions for submission, including a $40.00 payment requirement and the necessary accompanying documents. Importantly, it highlights the restrictions and allowances for the usage of the CPA title post-registration, which does not extend to the practice of public accountancy without further licensure. The form draws attention to the varied contexts in which the CPA title can be used by the registrant, such as personal stationary, within employment by a CPA or PA firm, by officers or employees in non-CPA firm industries, and by faculty members or administrators in educational institutions. Moreover, it delineates the legal boundaries of title usage in preventing unauthorized practice of public accountancy, underscoring the form's critical role in maintaining professional integrity and compliance within Connecticut's accounting sphere.

CPA CERTIFICATE REGISTRATION APPLICATION

Office of the Secretary of the State

Connecticut State Board of Accountancy

Form

For Board use only!

Check No.______________

Transaction Date____________

Amount Received____________

ID No. ____________________

GENERAL INSTRUCTIONS

Please type or print all requested information. Mail completed forms to State Board of Accountancy, Payment Center, P.O. Box 150477, Hartford, CT

Use this form only if you are the holder of a CPA Certificate and wish to register the Certificate in order to be allowed limited use of the title Certified Public Accountant & the initials CPA.

All applications for CPA Certificate Registration will be placed on the next available Board meeting agenda for approval (the Board typically meets monthly). The Certificate Registration is valid for the remainder of the calendar year in which it is granted (Jan. 1, - Dec. 31,).

Applicants are cautioned that the registration of the CPA Certificate does not grant the authority to practice public accountancy.

1.Applicants name as you wish it to appear in our records and address:

_____________________________________________

_____________________________________________

_____________________________________________

_____________________________________________

Home Ph ( ) -Work Ph ( ) -

Email address:_________________________________

______________________________________________

2.Provide your CPA Certificate Number and the issuing jurisdiction (State)

CPA Certificate Number___________

Issuing jurisdiction___________________________

Check this block if your CPA Certificate is listed under another name and provide below.

________________________________________

Other name:

______________________________________________

3. Sign & Date

________________________ |

__________ |

Applicant Signature |

Date |

Allowable use of the Title CPA by A Connecticut Registered

Certificate holder

Personal use

•On personal stationary

•On personal checks

•On social correspondence

Employees of a CPA or PA Firm (who are not proprietors, partners or shareholders) may use the title in the course of employment with such firm:

•In oral or written communication.

•In connection with the listing of the employee's name on the firm's letterhead or advertising, provided that such letterhead or advertising indicates that the employee is not a proprietor, partner or shareholder.

•On business cards which identify such firm.

Officer or employee of an entity other than a CPA firm

(Commonly called business and industry) may use the title only in connection with their association with the entity and only if such usage clearly identifies the entity and the person's position within such entity.

•In oral or written communication.

•In directories

•On business cards

•On letterhead

Faculty member or administrator of an educational institution may use the title in connection with such employment as a faculty member or administrator:

•In academic catalogues.

•In articles, books, and other publications.

•In directories or listings.

Registered Certificate holders may not affix their name or the name of any firm to a report, or affix the name of a firm or their name together with the title to any tax return, or practice public accountancy.

Section

Use of the title "Certified Public Accountant" upon registration of a certificate

(a)Definitions. As used in this section:

(1)"Certificate" means a Connecticut, "certified" public accountant" certificate issued either prior to October 1, 1992, or pursuant to section

(2)"Firm" means any person, proprietorship, partnership, corporation or association and any other legal entity that practices public accountancy;

(3)"License" means a public accountancy license issued pursuant to section

(4)"Licensee" means the holder of a certificate issued pursuant to section

(5)"Permit,” means a permit to practice public accountancy issued to a firm pursuant to section

(6)"Practicing public accountancy" means performing for the public or offering to perform for the public for a fee by a person or firm holding himself or itself out to the public as a licensee one or more kinds of services involving the use of accounting or auditing skills, including, but not limited to, the issuance of reports on financial statements, or of one or more kinds of management advisory, financial advisory or consulting services, or the preparation of tax returns of the furnishing of advice on tax matters;

(7)"Registration" or "Registered" means, when used in the context of a certificate, registration pursuant to subsection (f) of section

(8)"Report" means any writing which refers to a financial statement and (A) expresses or implies assurance as to the reliability of said financial statement, and includes, but is not limited to, any writing disclaiming an opinion, when such writing contains language conventionally understood in the profession to express or imply assurance as to the reliability of such financial statement, and (B) expresses or implies that the person or firm issuing such writing has special competence in accounting or auditing, which expression or implication arises from, among other things, the use of written language which is conventionally understood in the profession to express or imply assurance as to the reliability of financial statements.

(9)"Title pertaining to certification" or "Title pertaining to such certification" means the title or designation "certified public accountant" or the abbreviation "CPA" or any other title, designation, words, letters, abbreviations, sign, card or device tending to indicate that a person is a certified public accountant.

(b)The holder of a certificate who does not also hold a license shall not use the title pertaining to such certification except as permitted by this section of the regulations of the Connecticut state agencies.

(c)In addition to the use permitted by subsection (g) of this section, the holder of a registered certificate who is an employee of a firm which holds a current permit to practice public accountancy but who is not a proprietor, partner or shareholder of such firm, may use the title pertaining to such certification, only in the course of his employment with such firm, in oral or written communication, in connection with the listing of such employee's name on the firm's letterhead an in advertising for the firm, provided that such letterhead or advertising indicates that such employee is not a proprietor, partner or shareholder in such firm, and in connection with the listing of such employee's name on business cards which identify such firm.

(d)In addition to the use permitted by subsection (g) of this section, the holder of a registered certificate actively employed as a faculty member or administrator of an educational institution, whether public or private, for profit or nonprofit, may use the title pertaining to such certification only in connection with such employment as a faculty member or administrator, including ,but not limited to, use in academic catalogues, articles, books and other publication and in academic directories or listings.

(e)In addition to the use permitted by subsection (g) of this section, the holder of a registered certificate who is an officer or employee of an entity other than a firm engaged in the practice of public accountancy may use the title pertaining to such certification only in connection with his association with such entity and only if such usage clearly identifies the entity and the person's position within such entity, and may include use on correspondence, business cards, directories, and oral or written communication.

(f) . Nothing in this section shall be construed to allow the holder of a certificate, who does not also hold a license, to affix his name or the name of any firm to a report, or to affix the name of a firm or his name together with the title pertaining to such certification to any tax return, or to allow the holder of a certificate, who does not also hold a license and a permit, to practice public accountancy

(g)The holder of a certificate may use the title pertaining to such certification on personal stationary, checks and social correspondence, provided that, except as provided in subsections (c), (d) and (e) of this section, such title shall not be used in connection with any activity engaged in for the purpose of generating income or which does generate income.

| Fact Name | Description |

|---|---|

| Form Title | CPA Certificate Registration Application |

| Administering Body | Office of the Secretary of the State Connecticut State Board of Accountancy |

| Form Number | SBA-2 (Rev. 02/12) |

| Submission Address | State Board of Accountancy, Payment Center, P.O. Box 150477, Hartford, CT 06115-0477 |

| Payment Amount | $40.00 |

| Payment Methods | Check, Money Order, Cashier’s Check, Credit Card (with separate Credit Card Payment Sheet) |

| Usage of CPA Title | Limited use for personal, employment, and association purposes without implying authority to practice public accountancy |

| Application Approval | Applications reviewed at the next available Board meeting (Board typically meets monthly) |

| Registration Validity Period | Valid for the remainder of the calendar year in which it is granted (Jan. 1 - Dec. 31) |

| Governing Laws | Section 20-280-20 of the Connecticut State Board of Accountancy Regulations, sections 20-281c, 20-181b, and 20-281d of the Connecticut General Statutes |

Once you've decided to register your CPA Certificate in Connecticut, using the SBA-2 form is the next step you'll take to formally acknowledge your credential and its privileges within the state. While it might seem daunting at first, registering your certificate is straightforward once you understand the process. This certificate registration allows for the limited use of the Certified Public Accountant title and the initials CPA, under specific conditions detailed by the Connecticut State Board of Accountancy. Remember, however, that this registration does not grant authority to practice public accountancy.

Below are the detailed steps for completing the Connecticut SBA-2 form:

After completing these steps, remember these key points:

Completing the SBA-2 form is a valuable step for CPA Certificate holders in Connecticut, opening doors to using the CPA title under specific conditions while ensuring compliance with state regulations.

The Connecticut SBA-2 form is used for CPA Certificate Registration with the Connecticut State Board of Accountancy. It allows Certified Public Accountants to register their certificate so they may have limited usage of the title "CPA" and the initials "CPA" in the state. This application does not grant authority to practice public accountancy but permits the use of the title under specific conditions.

The completed SBA-2 form should be mailed to the State Board of Accountancy, Payment Center, P.O. Box 150477, Hartford, CT 06115-0477. A payment of $40.00 is required, which can be made by check, Money Order, or Cashier’s Check payable to the Treasurer State of Connecticut. For those opting to pay by credit card, a separate Credit Card Payment Sheet is required and can be downloaded from the website. This payment sheet must accompany the SBA-2 form.

Applications for CPA Certificate Registration are placed on the agenda of the next available Board meeting for approval. The Connecticut State Board of Accountancy typically meets on a monthly basis.

The registration is valid through the end of the calendar year in which it is granted, from January 1 to December 31. After this period, certificate holders must apply for renewal to maintain their registered status.

Yes, registered certificate holders cannot use their name or the firm’s name alongside the CPA title on reports, tax returns, or in the practice of public accountancy without holding both a license and a permit. The regulation is designed to ensure that only properly licensed individuals provide public accountancy services.

If your CPA Certificate is under a different name than what you are currently using, you must check the appropriate box on the form and provide the name under which your certificate is listed. This helps in accurate identification and registration of your credentials.

The Credit Card Payment Sheet required for those opting to pay the registration fee with a credit card is available for download on the Connecticut State Board of Accountancy’s website. Look under the forms section to find the necessary documentation.

Filling out the Connecticut SBA-2 form, a CPA Certificate Registration Application, is a crucial step for Certified Public Accountants (CPAs) wishing to register their certificates in Connecticut. However, applicants often make common mistakes that can delay or impact the registration process. Understanding and avoiding these mistakes is important for a smooth registration process.

To avoid these common mistakes, applicants should carefully read and follow all instructions on the form, double-check all provided information for accuracy, and ensure that all required documentation and payments accompany the form when submitted. Attention to detail and thoroughness can expedite the registration process and avoid unnecessary delays or complications.

When navigating the legal and regulatory requirements in Connecticut, especially for professionals like Certified Public Accountants (CPAs), understanding and submitting the correct forms is just the tip of the iceberg. The Connecticut SBA-2 form, or CPA Certificate Registration Application, serves as a key document for CPAs to register their certificates, enabling them to use the CPA title within the specified guidelines. However, this application often accompanies several other important documents, each playing a crucial role in ensuring compliance and securing the full benefits of CPA certification within the state.

The journey to becoming a registered CPA in Connecticut encompasses more than filling out and submitting the SBA-2 form. It involves a collection of documents that affirm the applicant's qualifications, ethical standing, and commitment to ongoing education in their field. Together, these forms create a comprehensive package that, once approved, grants the applicant the privilege of using the CPA designation—a mark of credibility and professionalism in the accounting industry. It's a meticulous process, but one that underscores the integrity and excellence expected of certified public accountants.

The Connecticut SBA-2 form, which is a CPA Certificate Registration Application used by the Office of the Secretary of the State Connecticut State Board of Accountancy, shares similarities with other professional licensure and certification forms in structure, purpose, and required information. Below are examples of forms that exhibit similarities to the SBA-2 form:

Uniform CPA Examination Application: Like the SBA-2 form, the Uniform CPA Examination Application is used by candidates who wish to become certified public accountants. Both documents require detailed personal information, educational qualifications, and professional experience. They serve as initial steps in the certification process, although the Examination Application is specifically for candidates seeking to take the CPA exam, while the SBA-2 form is for those who are already certificate holders and wish to register their certificate in Connecticut. The focus on ensuring applicant qualifications before proceeding in the respective processes is a common thread.

Licensing Application for Professional Engineers: This application, while for a different profession, is structured similarly to the SBA-2 form in its collection of applicant's personal information, professional history, and the requirement of a fee submitted alongside the application. Both forms are integral to the licensing and certification process within their respective fields, ensuring that only qualified individuals are granted the right to practice. They also underscore the importance of professional standards and public trust in these fields by restricting titles and practice to those properly registered or licensed.

When filling out the Connecticut SBA-2 form, it's essential to follow the guidelines precisely to ensure a smooth application process. Below are some recommended practices to adopt as well as some pitfalls to avoid:

Understanding the nuances of the Connecticut SBA-2 form, which details the CPA (Certified Public Accountant) Certificate Registration Application, is pivotal for professionals navigating the accounting landscape in Connecticut. Given the form’s complexity, misconceptions are common, leading to confusion and misunderstandings about its requirements and implications. Here, some of these misconceptions are clarified to aid in better comprehension and compliance.

Misconception 1: Registration grants authority to practice public accountancy. It's crucial to understand that registering your CPA certificate using the SBA-2 form does not authorize you to practice public accountancy. The form is designed solely for the purpose of allowing limited use of the CPA title and initials under specified conditions. This distinction is vital for compliance and professional conduct.

Misconception 2: The registration is permanent. Another common misunderstanding is the duration of the certificate registration. It's not lifelong; instead, it is valid only for the remainder of the calendar year in which it's granted. Certificate holders must renew their registration accordingly, ensuring they remain in good standing.

Misconception 3: Credit card payments can be made directly on the form. While the form mentions payment, it requires a separate Credit Card Payment Sheet for those opting to pay by credit card. This detail is often overlooked, leading to delays in the processing of registrations.

Misconception 4: Any form of the CPA title can be used upon registration. The use of the CPA title is notably restricted, even after registration. Certificate holders are limited in how and where they can use the CPA title, with clear stipulations provided on permissible usage, including restrictions on affixing the title to tax returns or reports, and specific guidelines for personal versus professional use.

Misconception 5: The form applies to all CPA certificate holders regardless of their state of issue. This form is specifically for those holding a CPA Certificate issued by or recognized in Connecticut. Certificate holders from other jurisdictions must ensure their certification is accepted by Connecticut before proceeding with the SBA-2 registration.

Misconception 6: Email and phone number are optional fields. All sections of the form, including contact information such as email address and phone number, are required unless explicitly stated. This information is crucial for communication and processing, and omitting it can result in incomplete application submissions.

Misconception 7: Registration allows the holder to use the CPA title in any context. The form outlines specific scenarios where the CPA title can be used by registered certificate holders, including on personal stationery, social correspondence, or in certain professional contexts that do not imply authority to practice public accountancy. The regulations aim to prevent misunderstanding regarding the professional capabilities and licensure of the certificate holder.

Misconception 8: Submitting the application guarantees approval. Completing and submitting the SBA-2 form is just the initial step. All applications are subject to approval by the Connecticut State Board of Accountancy. The review process ensures that applicants meet all the requirements for certificate registration.

Clarifying these misconceptions is crucial for CPA certificate holders planning to register their certificates in Connecticut. Understanding the proper scope of registration, the limitations on the use of the CPA title, and the procedural requirements of the SBA-2 form can streamline the registration process and ensure compliance with state regulations. Proper awareness and adherence to these guidelines protect both the certificate holder and the public by maintaining the integrity and professionalism of the accounting field.

Filling out and using the Connecticut SBA-2 form is an essential process for CPA Certificate holders in Connecticut who wish to register their Certificate. Here are eight key takeaways to guide you through the process:

Remember, accurate and complete submissions, along with adherence to the outlined use and restrictions of the title, are critical to ensuring compliance with the Connecticut State Board of Accountancy's regulations.

Connecticut W 1130 - It collects personal data such as name, address, and social security number for individuals seeking ABI waiver services.

How to Become a Teacher in Connecticut - The State Board of Education conducts criminal history and child abuse/neglect registry checks for all applicants, as noted on the ED 170 form.

Ct Change of Address Form - Designed with clarity to help residents navigate their DMV obligations with ease.